DEMAND & SUPPLY

Demand

It is the quantity of a good or service that customers are willing and able to purchase during a specified period under a given set of economic conditions.

Conditions to be considered include the price of the good in question, prices and availability of related goods, expectations of price changes, consumer incomes, consumer tastes and preferences, advertising expenditures, and so on.

The amount of the product that consumers are prepared to purchase, its demand, depends on all these factors.

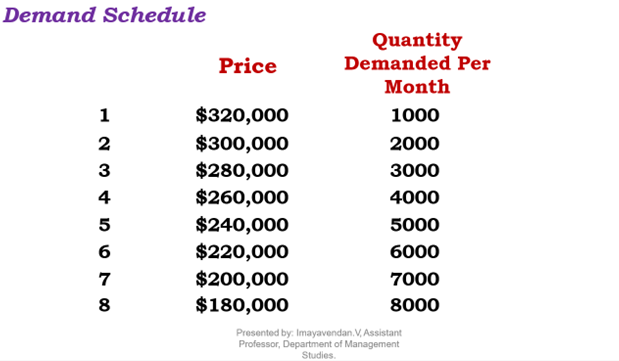

Demand Schedule

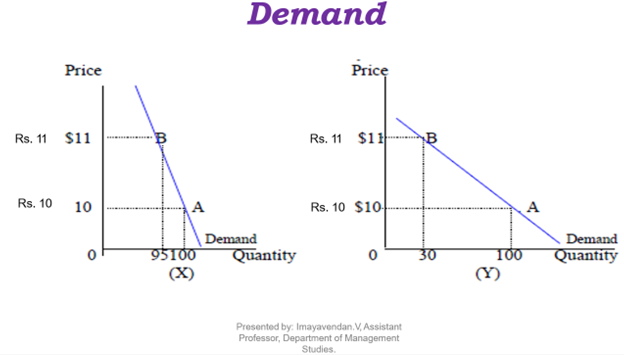

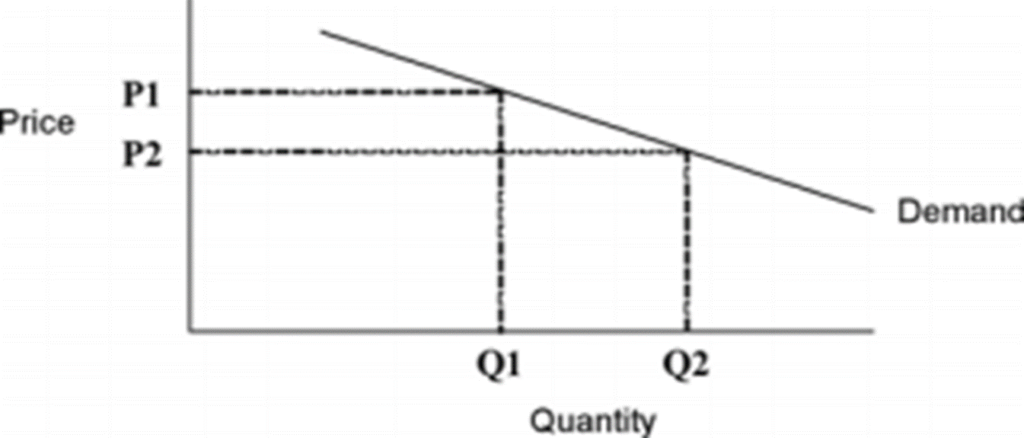

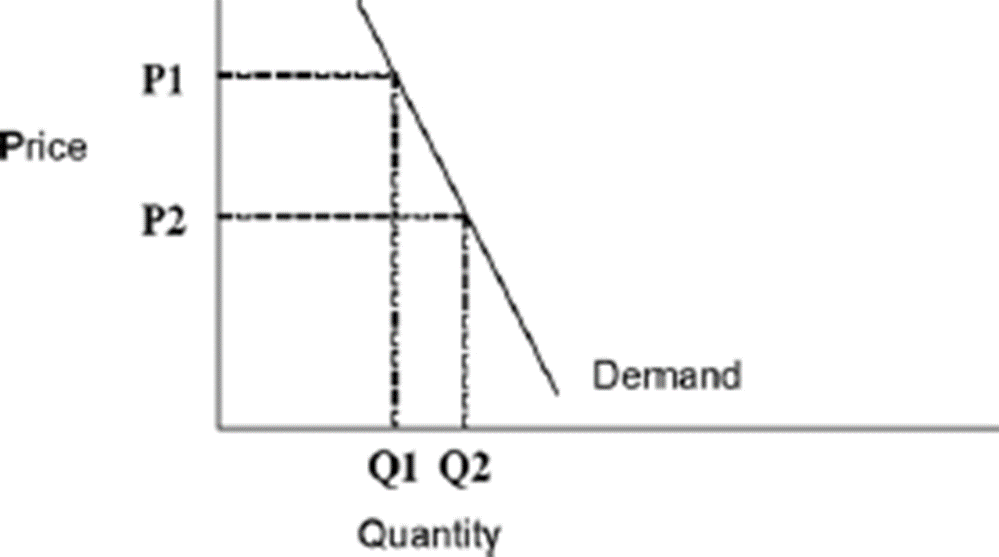

Law of Demand – there is an inverse relationship between price and quantity demanded.

as the quantity demanded rises, the price falls

as the price rises, the quantity demanded falls

as income rises, the demand for the product rises

as supply rises, the demand falls

Elasticity

Elasticity is a central concept in the theory of supply and demand.

In this context, elasticity refers to how supply and demand respond to various factors, including price as well as other stochastic principles.

One way to define elasticity is the percentage change in one variable divided by the percentage change in another variable.

Concept of Elasticity

Price Elasticity of Demand

Income Elasticity of Demand

Cross Elasticity of Demand

1. Price Elasticity of Demand

Price elasticity of demand is the change in quantity of a commodity demanded to the change in its price.

The degree of change in the demand of different commodities due to change in the price of the commodities may vary.

In certain cases, the changes in demand may be at higher rates.

Price elasticity of demand= Percentage change in quantity demanded/ Percentage change in price

2. Income Elasticity of Demand

Income Elasticity of demand is the degree of the responsiveness of demand to the change in income.

The income elasticity of demand is a measure of the extent to which the demand for a good changes when income changes, other things remaining the same.

Income elasticity of demand= Percentage change in quantity demanded / Percentage change in income.

3. Cross Elasticity of Demand

The responsiveness of demand to change in prices of related goods is called cross elasticity of demand (related goods may be substitutes or complementary goods).

In other words, it is the responsiveness of demand for commodity X to the change in the price of commodity Y.

Cross elasticity of demand= Percentage change in quantity demanded of a good./ Percentage change in price of one of its substitutes or complement

Elasticity Demand

Elastic

Inelastic

Unitary

1. Elastic Demand

An elastic demand is one in which the change in quantity demanded due to a change in price is large.

2. Inelastic Demand

An economic term used to describe the situation in which the supply and demand for a good or service are unaffected when the price of that good or service changes.

The most famous example of relatively inelastic demand is that for gasoline.

As the price of gasoline increases, the quantity demanded doesn’t decrease all that much.

This is because there are very few good substitutes for gasoline and consumers are still willing to buy it even at relatively high prices.

3. Unitary elastic

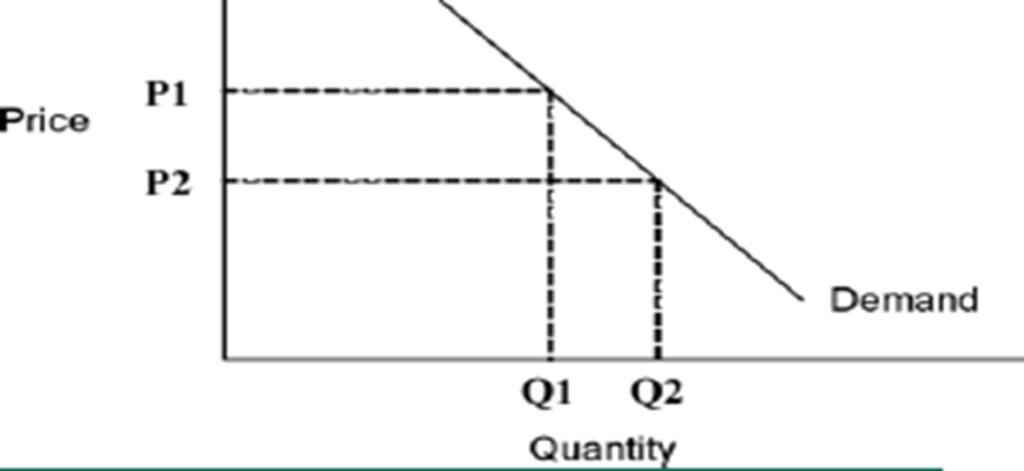

If the elasticity coefficient is equal to one, demand is unitarily elastic as shown in below figure.

For example, a 10% quantity change divided by 10 % price change is one. This means that a one percent change in quantity occurs for every one percent change in price.

3. Unitary elastic (Example)

Consider a situation in which milk costs Rs. 10 per liter. A grocer notices that he is not selling as much milk as he would like, so he puts the milk on sale, dropping the price to Rs. 7 per liter.

With unitary elasticity, the number of sales would double because the price was cut in half.

So if the grocer would sell 100 liter of milk at Rs. 10, that would lead to revenues of Rs. 1,200.

Cutting the price to Rs. 7 would then yield sales of 200 liter, still leading to revenues of Rs. 1,200 .

Determinants of Demand

Changes of Income

Changes of Taste or Preferences

Changes of Prices of Related Goods

Changes of Price Expectations

Changes of Size of Population

Look at the relationship between the quantity demanded and each of the determinants in turn – separately – price quantity relationship in the demand curve….

Factors Affecting Elasticity Of Demand

1.Availability of Substitutes

2.Postponement of Consumption

3.Proportion of Expenditure

4.Nature of the Commodity

5.Different Uses of the Commodity

6.Change in Income

7.Habits

8.Distribution of Income

9.Price Level

DEMAND FORECASTING

Demand forecasting is the activity of estimating the quantity of a product or service that consumers will purchase.

Demand forecasting involves techniques including both informal methods,

a)such as educated guesses, and quantitative methods,

b)such as the use of historical sales data or current data from test markets.

Necessity for forecasting demand

Often forecasting demand is confused with forecasting sales.

But, failing to forecast demand ignores two important phenomena.

There is a lot of debate in demand-planning literature about how to measure and represent historical demand, since the historical demand forms the basis of forecasting.

The main question is whether we should use the history of outbound shipments or customer orders or a combination of the two as proxy for the demand.

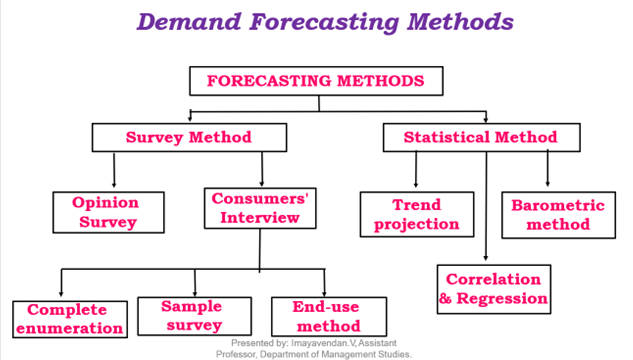

Demand Forecasting Methods

Concept of Supply

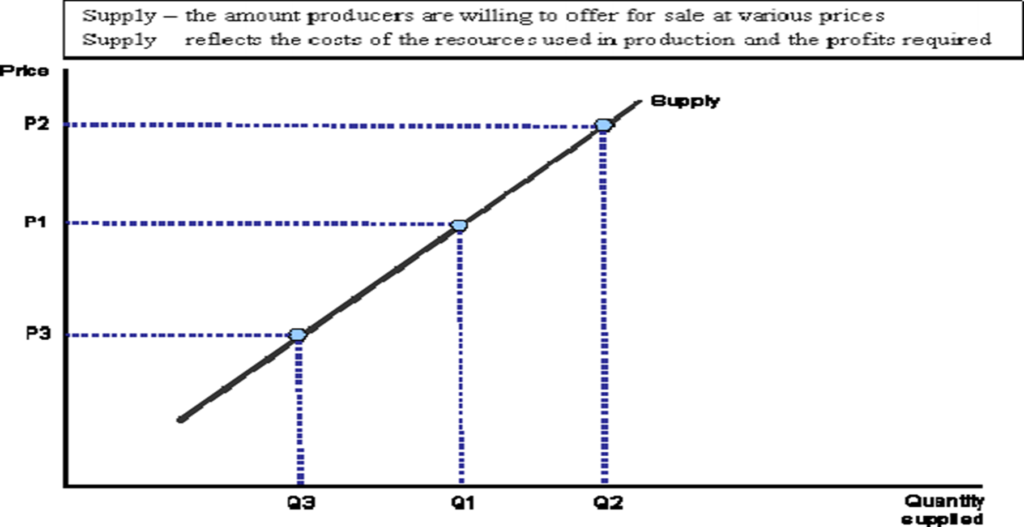

Supply is defined as the quantity of a product that a producer is willing and able to supply onto the market at a given price in a given time period.Note: Throughout this study companion, the terms firm, business, producer and seller have the same meaning.

Supply is the amount of a good that producers are willing and able to offer for sale at various price.

The law of Supply

All else equal, the quantity supplied is positively related to price.

Increase in Prices Increase in quantity supplied

Increase in Prices Increase in quantity supplied

The law of supply explains that if people are willing to pay more money for a product, a company will produce or manufacturemoreof that product to capitalize on the increased revenue.

The opposite also holds true that as the price of a product drops, a company is likely to manufacture less of that product.

In fact, if sales drop too far, the company may discontinue the product altogether.

Determinants of Supply

•Market price

•Input prices

•Technology (new production methods)

•Expectations Number of producers

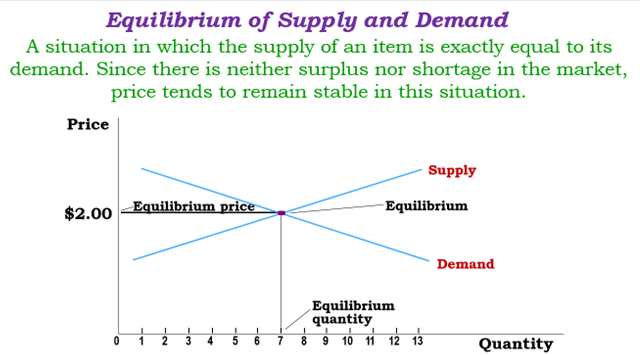

Equilibrium of Supply and Demand

A situation in which the supply of an item is exactly equal to its demand. Since there is neither surplus nor shortage in the market, price tends to remain stable in this situation.